Why stablecoins beat traditional wires in LATAM

For millions of families in Mexico, Colombia, and Brazil, sending money home is a monthly necessity, not a luxury. The economic case for stablecoins is now clear: they offer a faster, significantly cheaper alternative to legacy banking rails. A 2026 survey of 4,600 users across 15 Latin American countries found that stablecoin transfers cost an average of 40% less than traditional remittance channels. This reduction is not marginal; it is a structural advantage that directly impacts household income in a region where remittances are a critical economic pillar.

The timing for this shift is driven by both regulatory changes and technological maturity. With the new remittance tax in the United States taking effect in January 2026, migrants are increasingly seeking cheaper alternatives to avoid eroding their earnings. Traditional wire transfers, with their hidden intermediary fees and slow settlement times, are becoming less viable for cost-conscious senders. Stablecoins, by contrast, settle on-chain in minutes, bypassing the multi-day delays typical of SWIFT networks.

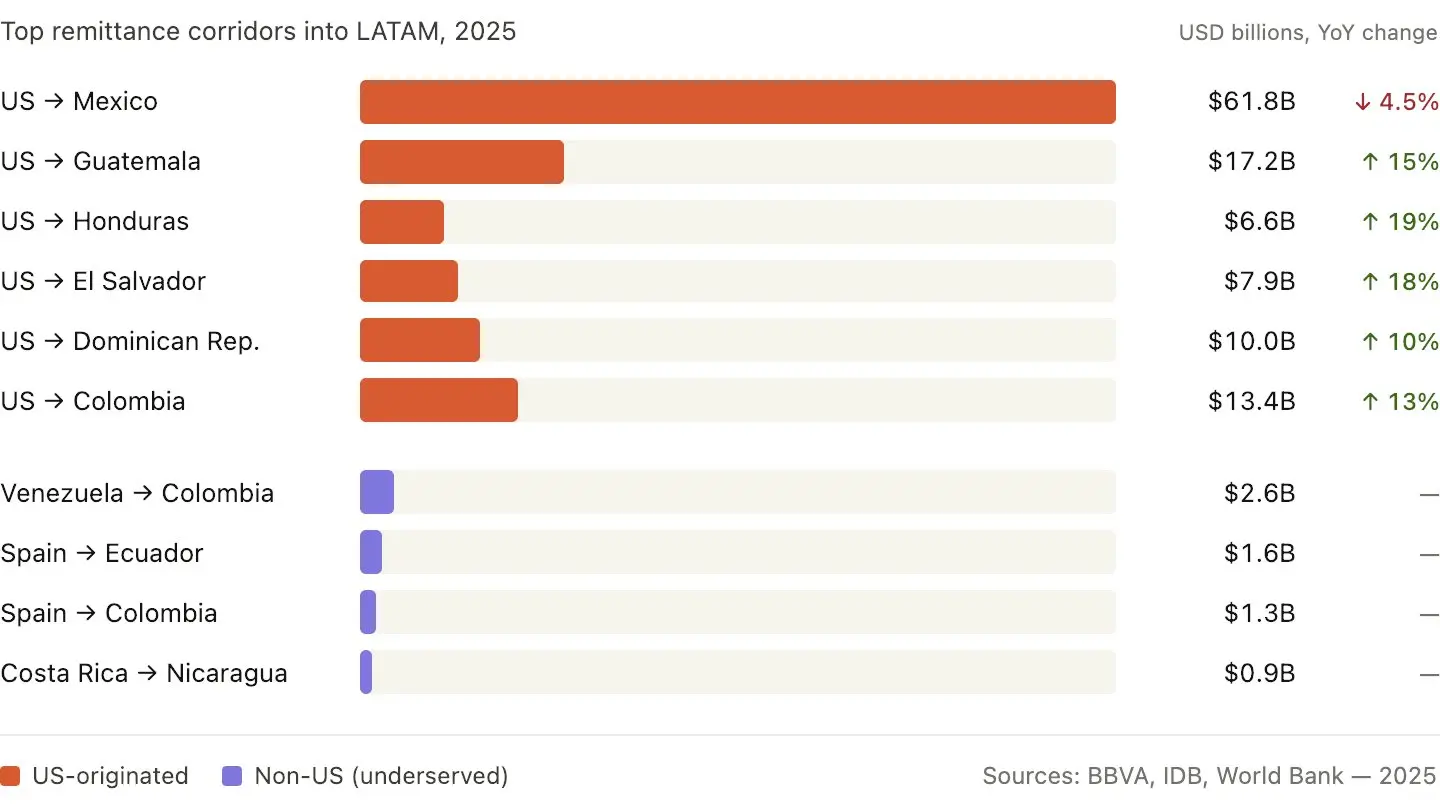

Mexico remains the region's leading recipient of remittances, with $65 billion expected this year. In corridors like Mexico-US, Colombia-US, and Brazil-US, the speed and transparency of stablecoin networks offer a tangible improvement over legacy systems. Users retain control over their funds until the moment of transfer, reducing the risk of lost or misdirected payments. This clarity, combined with lower costs, makes stablecoins the practical choice for modern cross-border payments.

As an Amazon Associate, we may earn from qualifying purchases.

Top stablecoin remittance providers ranked

Selecting the right stablecoin remittance provider in LATAM requires balancing speed, liquidity, and regulatory compliance. The market has shifted from experimental pilots to established corridors, with Mexico, Colombia, and Brazil leading adoption. Providers now compete on direct integration with local payout rails like SPEI (Mexico), PSE (Colombia), and Pix (Brazil), ensuring that stablecoins settle as fiat in recipients' bank accounts within minutes.

The following providers are ranked based on their ability to handle high-volume cross-border flows with minimal friction. Each offers distinct advantages depending on the corridor and the volume of transfers.

1. Mural Pay

Mural Pay has emerged as a leader in Latin American stablecoin infrastructure, focusing on B2B and B2C remittance corridors. Their platform specializes in converting USDC and USDT into local fiat via Pix in Brazil and SPEI in Mexico. Mural Pay is particularly strong for businesses and high-volume senders due to its deep integration with local banking partners, which reduces the risk of transaction failures and ensures faster settlement times compared to generic crypto exchanges.

2. Tazapay

Tazapay provides a robust compliance framework that is essential for institutional players entering the LATAM market. Their technology allows for seamless cross-border payouts while adhering to strict KYC/AML regulations in Brazil, Mexico, and Argentina. Tazapay is ideal for financial institutions and large fintechs that prioritize regulatory safety and liquidity management over consumer-facing simplicity. They support major stablecoins and offer API-driven solutions for automated payroll and vendor payments.

3. Wally

Wally operates as a digital wallet and payment gateway that simplifies the on-ramp and off-ramp process for individual users and small businesses. Available in Mexico, Colombia, and Peru, Wally allows users to send and receive stablecoins with ease, converting them to local currency instantly. The platform's user experience is designed for non-technical users, making it a practical choice for personal remittances where speed and ease of use are the primary concerns.

Comparison of Key Providers

The table below summarizes the core differences between the leading stablecoin remittance tools for LATAM.

| Provider | Fee Structure | Settlement Time | Local Payout Methods |

|---|---|---|---|

| Mural Pay | Competitive, volume-based | < 10 minutes | Pix, SPEI, PSE |

| Tazapay | Institutional tiers | < 15 minutes | SPEI, Pix, Bank Transfer |

| Wally | Fixed low fee | < 5 minutes | Pix, SPEI, Mobile Wallets |

Security and Hardware Recommendations

Given the high stakes of cross-border financial transfers, securing your private keys is non-negotiable. If you are managing significant volumes of stablecoins, consider using a hardware wallet to store your assets offline. The following products are commonly used by LATAM remittance professionals to secure their funds.

As an Amazon Associate, we may earn from qualifying purchases.

How the 2026 US remittance tax affects payouts

Starting January 2026, the United States imposes a 1% federal excise tax on cross-border remittances. This rule applies to transfers sent from the US to Mexico, Colombia, Brazil, and other countries. It is a US federal requirement, not a local tax in the receiving country. The tax applies to the total amount sent, meaning the full $500 sent is taxed, not just the fee portion.

For stablecoin users, this creates a new cost layer. Traditional money transfer services often bundle fees and exchange rates, making the tax impact less visible. With stablecoins, the 1% is a direct deduction from the principal. If you send $1,000, the sender or receiver may see $10 withheld depending on how the remittance provider structures the transaction. This reduces the net amount received in LATAM.

This change is driving a shift in how migrants view digital assets. Many are moving away from traditional corridors that do not clearly disclose this new cost. The goal is to find tools that either absorb the tax or make it transparent. For families in Mexico, who receive the largest share of remittances in the region, even a 1% reduction adds up significantly over the year.

As an Amazon Associate, we may earn from qualifying purchases.

Choosing the right network for speed and cost

Selecting a blockchain for remittances in Latin America is less about hype and more about matching the network’s economics to the specific corridor. The best stablecoin remittance tools for LATAM in 2026 rely on chains that offer near-zero fees and fast finality, ensuring that the sender’s money actually reaches the recipient without being eaten by gas costs or delayed by slow block times.

Polygon stands out for its deep integration with existing financial infrastructure, particularly for larger transfers. Banks in the region are cutting cross-border payment costs by 30–50% using Polygon’s stablecoin rails, making it a reliable choice for corridors like Mexico, which receives the highest volume of remittances in the region at $65 billion annually. The network’s low fees make it efficient for both small daily transfers and larger institutional flows.

Solana and Tron offer distinct advantages for speed and accessibility. Solana’s high throughput provides near-instant finality, ideal for users who need funds available immediately in countries like Colombia. Tron, specifically through USDT, remains dominant in Brazil due to its widespread adoption and low transaction costs, aligning with Brazil’s clear regulatory framework for virtual assets.

When evaluating these options, consider the transfer size and the recipient’s preferred withdrawal method. For high-value transfers, Polygon’s liquidity and bank partnerships provide stability. For rapid, frequent small transfers, Solana’s speed or Tron’s USDT ubiquity may be more practical.

Compliance and KYC requirements in LATAM

Stablecoin remittance providers operating in Mexico, Brazil, and Colombia must adhere to strict Anti-Money Laundering (AML) and Know Your Customer (KYC) standards. These regulations are not optional; they are the gatekeepers that determine whether funds reach recipients or get frozen by financial institutions.

In Mexico, providers must comply with the Federal Law for the Prevention and Identification of Operations with Resources of Illegal Origin. This requires robust identity verification for both senders and receivers, particularly for transactions exceeding certain thresholds. Major platforms often integrate local identity databases to verify sender details instantly, reducing the risk of fraudulent accounts.

Brazil’s Legal Framework for Virtual Assets (Law 14,478/2022) places significant oversight on virtual asset service providers. Providers must register with the Central Bank of Brazil and implement rigorous due diligence processes. This includes verifying the identity of users and monitoring transactions for suspicious activity. Failure to comply can result in heavy fines and suspension of services.

Colombia has also tightened its regulations, with the Financial Information and Analysis Unit (UIAF) requiring all virtual asset service providers to register and report suspicious transactions. Providers must ensure that their KYC processes meet international standards set by the Financial Action Task Force (FATF). This includes verifying the identity of users and maintaining records of transactions for at least five years.

To ensure compliance, many providers use third-party KYC services that verify identities through government-issued documents and biometric data. These services help providers meet regulatory requirements while minimizing the friction for users. Always choose a provider that clearly outlines its compliance measures and has a track record of adhering to local regulations.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!