New 1% remittance tax changes the math

Starting January 1, 2026, a new 1% federal tax applies to remittance transfers sent from the United States to recipients in foreign countries. This provision, part of the One Big Beautiful Bill, marks the first time the U.S. has directly taxed these cross-border flows.

The Inter-American Development Bank estimates that $161 billion was sent back to Latin America and the Caribbean in 2024, with Mexico alone receiving $65 billion. For families relying on these funds, even a small percentage adds up to significant cost. However, the tax's limited scope means that digital and stablecoin methods often remain more cost-effective than traditional cash-based services, which already carry higher fees.

While the tax is a new layer of cost, it primarily targets physical payment methods. This creates a clear incentive to shift toward digital channels that bypass the tax entirely, preserving more value for recipients in Latin America.

Top platforms for sending USDC to LATAM

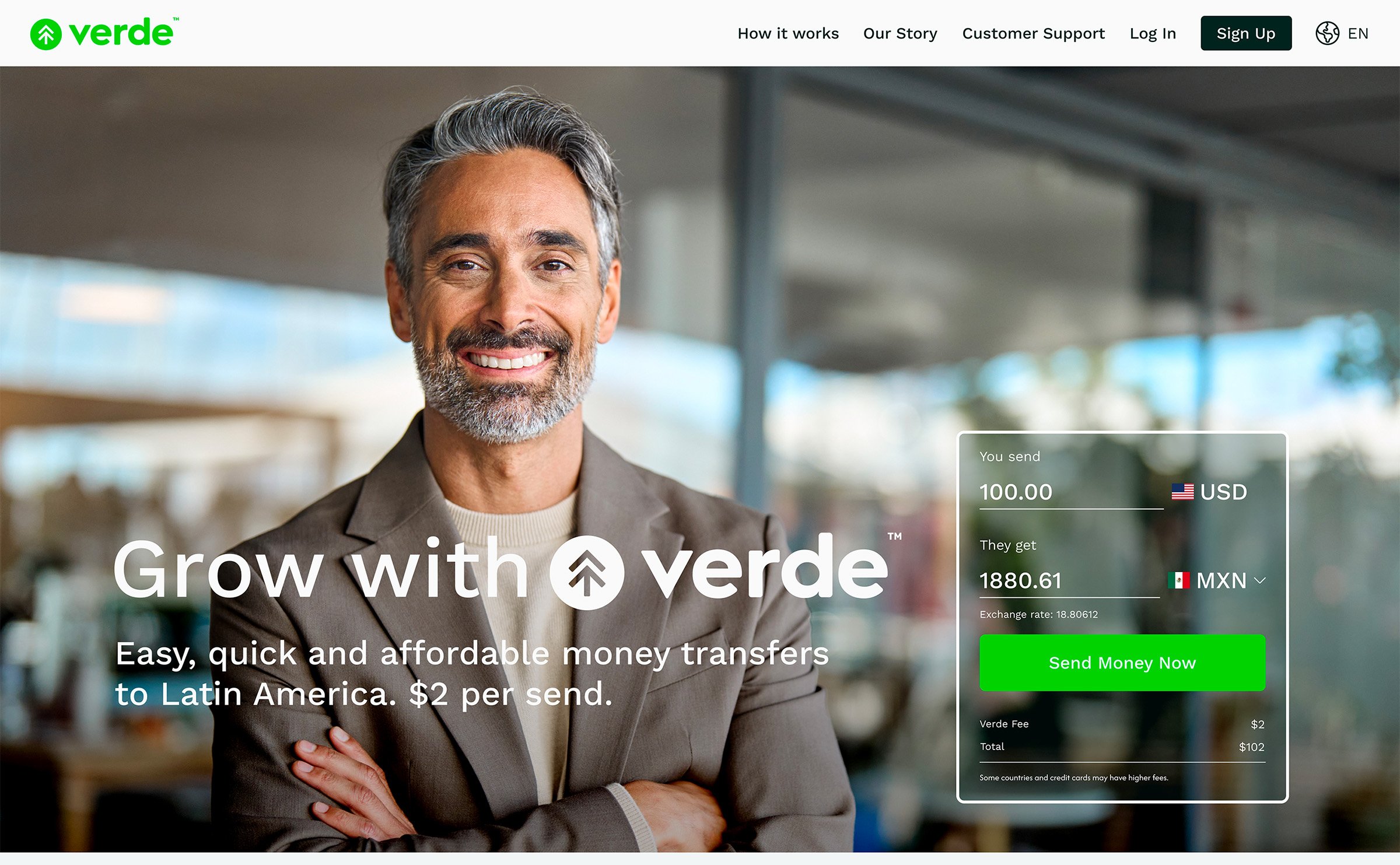

Sending USDC to Latin America requires navigating distinct regulatory environments and currency pressures. Platforms like Bitso, Binance Pay, and Crypto.com offer different pathways for moving value, but the choice depends heavily on the recipient's country and the sender's preferred compliance level. As of 2026, the new 1% remittance transfer tax on cash-based transfers from the United States makes digital stablecoin alternatives increasingly relevant for those seeking to avoid physical instrument fees, though stablecoin transfers remain subject to their own platform-specific costs and local tax obligations.

Bitso operates as a licensed digital asset exchange in Mexico, Colombia, and Argentina. It provides a regulated on-ramp for USDC, allowing users to convert fiat to stablecoins and send them directly to Bitso wallets. This approach offers a layer of regulatory oversight that appeals to users concerned with compliance, particularly in jurisdictions with strict financial monitoring. However, withdrawal fees and local banking integration can vary significantly between countries.

Binance Pay facilitates peer-to-peer (P2P) transfers of USDT and USDC without traditional banking intermediaries. Its P2P marketplace allows users to find counterparties who accept local payment methods, such as bank transfers or mobile wallets, creating a flexible but less centralized liquidity pool. While speed is often high, the lack of a direct fiat on-ramp within the core app for all regions means users must rely on third-party merchants, introducing counterparty risk that is absent in fully regulated exchanges.

Crypto.com offers a hybrid model with its Visa card ecosystem and global transfer features. Users can hold USDC and convert it to local fiat for spending or transfer it to other Crypto.com users instantly. The platform's strength lies in its integrated financial suite, but international transfer speeds and fees depend on the underlying blockchain network used (e.g., Ethereum vs. CRO Chain). Users must carefully select low-fee networks to avoid eroding the value of small remittances.

The following table compares the core operational metrics for these platforms. Note that fees and speeds are dynamic and depend on network congestion and local banking partners.

| Platform | Type | Speed | Regulation |

|---|---|---|---|

| Bitso | Licensed Exchange | 1-3 days (fiat withdrawal) | High (Local Licenses) |

| Binance Pay | P2P Marketplace | Minutes (P2P) | Medium (Global) |

| Crypto.com | Hybrid Ecosystem | Instant (internal) | High (Global Licenses) |

Regulatory clarity remains the primary differentiator. In Argentina, where inflation and currency controls are severe, Bitso's local licensing provides a safer conduit for holding value in USDC compared to unregulated P2P channels. In Colombia, where digital adoption is high, Binance Pay's P2P network offers greater liquidity for smaller transactions. Senders should verify that their chosen platform complies with both their home country's AML/KYC rules and the recipient's local financial regulations.

Best fiat services for traditional transfers

Western Union, Wise, and Remitly remain the dominant fiat channels for sending money to Latin America. These platforms cater to recipients who require immediate cash pickup at physical agent locations or direct deposits into local bank accounts. Unlike digital-first stablecoin solutions, these services operate within the traditional banking infrastructure, offering familiarity and established physical networks across the region.

The landscape shifts significantly with the new 1% remittance transfer tax taking effect January 1, 2026. This tax applies specifically when senders use cash, money orders, or cashier’s checks to fund the transfer. For traditional fiat services, this means cash-funded transactions will incur an additional cost layer that digital bank transfers or card payments do not. Western Union and Remitly have updated their user interfaces to highlight these funding method distinctions, urging users to select bank-linked funding to avoid the surcharge.

Wise continues to differentiate itself by prioritizing bank-to-bank transfers with transparent fee structures. While it lacks the extensive cash pickup network of Western Union, Wise offers lower exchange rate markups for digital payments. Remitly sits in the middle, offering both cash pickup and bank deposit options with a focus on speed for first-time users. For readers relying on physical cash transactions due to unbanked recipients, the new tax represents a tangible increase in cost that must be factored into the transfer amount.

As an Amazon Associate, we may earn from qualifying purchases.

Choosing the right method for your corridor

Selecting a remittance platform requires matching the payment infrastructure to the recipient’s local economic reality. In 2026, the landscape is split between high-volume fiat corridors and inflation-resistant stablecoin networks. Your choice depends on whether the recipient needs immediate cash liquidity or long-term value preservation.

Mexico favors established fiat networks

Mexico remains the largest recipient of remittances in Latin America, with flows projected to reach $65 billion in 2026 [1]. The infrastructure here is mature, dominated by major banks and traditional money transfer operators. For recipients who need cash immediately or prefer to deposit directly into traditional bank accounts, fiat networks like Western Union or MoneyGram offer the most reliable access. The volume of transactions supports lower fees for larger amounts, making traditional corridors cost-effective for standard transfers.

Argentina requires stablecoin alternatives

In contrast, Argentina’s high inflation and strict currency controls make traditional fiat transfers risky for value preservation. Sending US dollars via a bank transfer often results in significant loss of value due to exchange rate spreads and local restrictions. Stablecoins like USDC or USDT provide a more efficient alternative. Recipients can receive funds on-chain and convert them to local currency at market rates, bypassing the official exchange distortions. This method is essential for maintaining purchasing power in hyperinflationary environments.

The 2026 remittance tax impact

A new 1% remittance transfer tax begins January 1, 2026, for transfers from the United States paid with cash, money orders, or cashier's checks [2]. This tax directly increases the cost of traditional cash-based corridors. If you frequently send small amounts in cash, switching to a bank-funded transfer or a digital stablecoin platform may mitigate this additional cost. Always verify the payment method's tax implications before finalizing your transfer.

Frequently asked questions about 2026 remittances

What is the remittance law for 2026?

Beginning January 1, 2026, a 1% federal tax applies to remittance transfers sent from the United States to foreign countries. This tax, enacted under the "One Big Beautiful Bill," specifically targets transactions where the sender provides cash, money orders, cashier's checks, or similar physical instruments to the provider. Digital payments using bank accounts or credit cards remain exempt from this levy.

What is the top remittance receiving country in Latin America?

Mexico remains the region's leading recipient, with projections indicating it will receive approximately $65 billion in 2026. This represents a 2.9% increase compared to 2023 levels. Meanwhile, Central American countries are seeing stronger growth, with remittances expected to rise by 6.6%, reaching a total of $45.7 billion for the region.

What is the economic outlook for Latin America in 2026?

The economies of Latin America and the Caribbean are projected to grow by 2.2% on average in 2026, according to the Economic Commission for Latin America and the Caribbean (ECLAC). This figure reflects a slight downward revision from the 2.3% estimated in December 2025, driven by diminishing annual changes in global money flows and regional economic adjustments.

Can you send money to another country in 2026?

Yes, international transfers continue, but the new 1% tax on cash-based remittances changes the cost structure. If you pay with physical instruments like cash or cashier's checks, you will incur the tax. To avoid this additional cost, many senders are switching to digital methods, such as direct bank transfers or stablecoin platforms, which are not subject to this specific federal levy.

No comments yet. Be the first to share your thoughts!