2026 marks the tipping point for stablecoin remittance LATAM

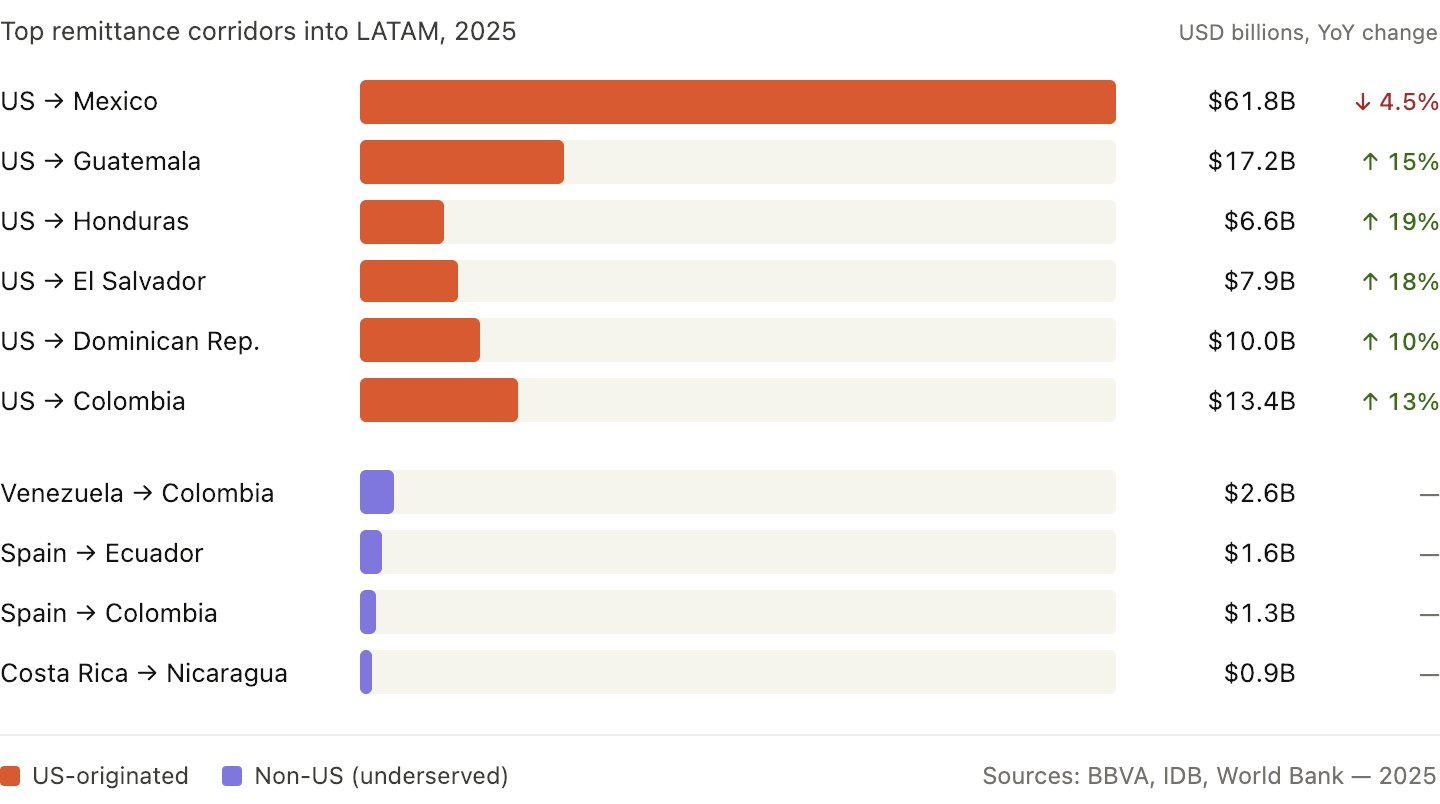

The landscape of cross-border payments in Latin America is undergoing a structural shift. Stablecoin remittance LATAM 2026 is no longer a niche experiment but a mainstream infrastructure layer, driven by regulatory clarity and relentless cost pressure. By 2026, stablecoins are projected to account for 18% to 22% of the remittance market, equating to roughly $25.5 billion to $31.2 billion in transfer volume [src-serp-2].

This transition mirrors a broader migration from crypto-native experimentation to core financial utility. The 2026 Stablecoin Momentum Report from ZeroHash highlights that this segment has crossed a critical threshold, moving into the realm of essential economic infrastructure [src-serp-3]. With annual remittance flows across Latin America reaching $142 billion, the increasing adoption of stablecoins represents a significant reallocation of capital toward more efficient settlement rails [src-serp-8].

The drivers are clear. Traditional remittance corridors, particularly those involving Mexico and Nicaragua, face high friction and fees. Stablecoins offer a way to reduce this friction by allowing senders to convert local currency into a digital asset, transmit it across a blockchain network within minutes, and have recipients convert it back to local currency [src-serp-4]. As regulatory frameworks like Brazil's Legal Framework for Virtual Assets provide oversight, compliance becomes standardized, further encouraging institutional and retail adoption.

Costs: Stablecoins vs traditional banks

For families sending money home, the difference between traditional wire transfers and stablecoin remittance LATAM 2026 models often comes down to two numbers: the upfront fee and the hidden spread. Traditional banks charge high fixed fees for cross-border transactions and apply unfavorable exchange rates that can eat up 5% to 10% of the total amount sent. In contrast, stablecoin rails like USDC and USDT operate on public blockchains where transaction costs are typically fractions of a cent, regardless of the amount.

The speed of settlement is the other major differentiator. A standard SWIFT wire transfer often takes two to five business days to clear, especially when involving intermediary banks in different jurisdictions. Stablecoin transfers settle in minutes, 24 hours a day, seven days a week. This speed reduces the risk of lost funds and allows recipients to access capital immediately for urgent needs.

The following comparison breaks down the typical costs and timelines for major LATAM corridors, including Mexico, Colombia, and Peru. These figures represent average market conditions for a $500 transfer, highlighting the structural advantages of digital asset rails over legacy banking systems.

| Corridor | Method | Avg. Fee | Settlement | FX Spread |

|---|---|---|---|---|

| Mexico | SWIFT Wire | $25–$45 | 2–5 days | 3–5% |

| Mexico | USDC/USDT | <$0.10 | <10 mins | 0.1–0.5% |

| Colombia | SWIFT Wire | $30–$50 | 3–5 days | 4–6% |

| Colombia | USDC/USDT | <$0.10 | <10 mins | 0.1–0.5% |

| Peru | SWIFT Wire | $25–$40 | 2–4 days | 3–5% |

| Peru | USDC/USDT | <$0.10 | <10 mins | 0.1–0.5% |

While the table above illustrates the stark contrast in direct costs, it is important to note that stablecoin adoption requires a degree of digital literacy. Recipients must have access to a crypto wallet and a local exchange to convert the digital assets into local currency. However, as on-ramp and off-ramp services in LATAM expand, this friction is decreasing, making the cost savings increasingly accessible to the average household.

The financial impact of these savings is significant. For migrant families sending money regularly, the difference between a $40 bank fee and a $0.10 stablecoin fee represents substantial cumulative savings over a year. This efficiency is driving a shift in how cross-border payments are viewed in the region, with stablecoins emerging as a viable alternative to traditional banking infrastructure for both individuals and enterprises.

The regulatory landscape across key markets

The rules for stablecoin remittance LATAM 2026 are no longer theoretical. They are being written now, and they vary sharply between the region’s largest economies. For remittance providers, compliance is not just about avoiding fines; it is the gatekeeper to market access.

Brazil’s formalized framework

Brazil has moved from experimentation to formalization. The Legal Framework for Virtual Assets (Lei dos Criptoativos), signed in late 2022, established the Central Bank of Brazil (BCB) as the primary regulator. By 2026, the BCB’s Resolution 5,899 is fully operational, requiring stablecoin issuers to maintain strict reserve transparency and robust AML/KYC protocols.

For remittance providers, this means integrating with BCB-licensed Virtual Asset Service Providers (VASPs). The system favors stability and traceability. Providers must ensure that every transaction is reported to the Financial Activities Report (RARF) system. This creates a clear, albeit bureaucratic, path to legitimacy for cross-border payments.

Mexico’s evolving oversight

Mexico’s approach is more cautious but increasingly structured. The National Banking and Securities Commission (CNBV) has been expanding its oversight of virtual asset service providers under the Financial Technology Institutions Law (LIFTI). In 2026, the focus is on preventing money laundering and ensuring that stablecoin issuers hold sufficient liquidity to back their tokens.

Remittance providers operating in Mexico must register with the CNBV and adhere to strict data localization rules. While the framework is less prescriptive than Brazil’s, the enforcement is tightening. Providers that fail to implement real-time transaction monitoring face significant penalties, making compliance a core operational cost rather than an afterthought.

Argentina’s adaptive measures

Argentina’s regulatory environment is shaped by its macroeconomic volatility. The Central Bank of Argentina (BCRA) has issued specific guidelines for virtual assets, emphasizing consumer protection and capital flow management. In 2026, the focus is on ensuring that stablecoin remittances do not bypass capital controls or facilitate illicit flows.

Providers must navigate a complex web of exchange rate regulations. While stablecoins offer a way to bypass traditional banking delays, they must still comply with BCRA reporting requirements. This creates a unique challenge: providers must balance the speed of blockchain settlement with the slower, more rigid requirements of traditional financial oversight.

Market data and price stability

Stablecoin remittance LATAM 2026 relies on the predictability of digital dollars. Unlike volatile crypto assets, stablecoins like USDC and USDT maintain a 1:1 peg to the US dollar. This stability is the primary reason enterprises and individuals are adopting them for cross-border payments. By avoiding the price swings of Bitcoin or Ethereum, senders protect their purchasing power, ensuring that the money arriving in families' hands is exactly what was sent.

The market has shifted from experimentation to core infrastructure. According to the 2026 Stablecoin Momentum Report, stablecoins have crossed a critical threshold in utility and adoption. This growth is driven by the need for speed and lower costs in corridors like Mexico and Brazil, where traditional wires are slow and expensive. The following chart illustrates the consistent stability of USDC against the dollar over the last 90 days.

Live market data confirms that these assets remain tightly pegged, providing a reliable settlement layer. This reliability is crucial for the billions of dollars in remittances flowing into Latin America annually. As regulations tighten and banks integrate stablecoin rails, the focus remains on preserving value while reducing friction.

Choosing a compliant stablecoin remittance LATAM 2026 path

Selecting a provider for stablecoin remittance LATAM 2026 requires verifying that the platform operates within local regulatory frameworks while minimizing hidden costs. The regulatory landscape in Mexico, Brazil, and Argentina has shifted toward strict AML and KYC enforcement. Providers that ignore these rules risk freezing funds or facing legal penalties. Prioritize platforms that explicitly publish their compliance status and partner with licensed local exchanges for fiat on-ramps and off-ramps.

Check if the provider holds licenses in your target country. In Brazil, regulators require strict reporting, while Mexico’s CNBV oversees virtual asset service providers. Avoid offshore-only platforms that lack local legal standing.

Ensure the platform enforces identity verification for both senders and receivers. Strong KYC processes reduce the risk of account freezes and ensure your remittance flow remains uninterrupted under 2026 compliance standards.

Look beyond the platform’s transaction fee. Calculate the total cost by adding network gas fees and the spread between the stablecoin price and local currency. Use a live comparison to see how fees impact the final amount received.

| Feature | Top-Tier Provider | Low-Cost Platform |

|---|---|---|

| Regulatory License | Yes (Local & International) | Often Offshore Only |

| KYC/AML | Strict Biometric Verification | Minimal or None |

| Fee Transparency | Detailed Breakdown | Hidden Spreads |

| Fiat On/Off-Ramp | Direct Bank Integration | Third-Party P2P |

No comments yet. Be the first to share your thoughts!