Why stablecoins beat traditional transfers

Sending money to Latin America in 2026 means navigating a landscape where traditional banking rails are becoming increasingly expensive and slow. For decades, SWIFT transfers have been the standard, but they often come with hidden costs: a 1% to 3% fee and a delivery window of three to five business days. By the time the funds arrive, exchange rate fluctuations and intermediary bank charges have already eroded the value of the remittance.

Stablecoins solve these friction points by operating on blockchain networks that settle in minutes rather than days, with fees often less than a dollar regardless of the transfer size. This speed and cost efficiency are critical for families who rely on regular remittances to cover essential needs. While the volume of money flowing to Latin America and the Caribbean is projected to increase slightly in 2026, the cost of moving that money should not rise proportionally. Stablecoins allow senders to keep more of their hard-earned dollars in the pockets of their recipients.

The choice between traditional banks and stablecoins is no longer just about technology; it is about financial efficiency. With the new 2026 tax on cash-based transfers, using digital assets offers a clear advantage in preserving the full value of the transfer. For anyone looking to send money to Latin America 2026, stablecoins provide a faster, cheaper, and more transparent alternative to the legacy banking system.

Choose the right stablecoin for LATAM

When you send money to Latin America 2026 using stablecoins, the choice between Tether (USDT) and USD Coin (USDC) determines how fast your recipient gets paid and how much they keep. While both tokens maintain a 1:1 peg to the US dollar, their liquidity profiles in Latin American markets differ significantly.

USDT is the dominant choice for most cross-border transfers to the region. It has the deepest liquidity in local exchange pairs across Colombia, Peru, and Brazil. This means local exchanges and peer-to-peer (P2P) platforms can convert USDT to local currency (COP, PEN, BRL) with minimal slippage and faster settlement times. For recipients, speed and availability are often more valuable than the secondary security features that USDC offers.

USDC is regulated and fully backed by US treasuries, making it a safer hold for long-term storage. However, it often faces lower liquidity on regional P2P markets. When you try to cash out USDC in LATAM, you may encounter wider spreads or longer wait times as local merchants scramble to find buyers. For a quick remittance, this friction costs time and money.

Use this comparison to decide which asset fits your transfer speed and recipient needs.

| Feature | USDT | USDC |

|---|---|---|

| LATAM Liquidity | High (Dominant) | Moderate |

| P2P Acceptance | Widespread | Limited |

| Regulatory Clarity | Lower (Offshore origins) | High (US Regulated) |

| Cash-Out Speed | Fast | Slower |

If your recipient needs cash within hours, USDT is the pragmatic choice. If you are storing funds for months before sending, USDC provides better regulatory peace of mind. Always verify which asset your local exchange supports before initiating the transfer.

-

Confirm recipient's local exchange accepts USDT or USDC

-

Check current spread for your specific currency pair

-

Verify network fees (ERC20 vs TRC20) to minimize costs

Step 1: Buy stablecoins on a regulated exchange

Before you can send money to Latin America 2026 using crypto, you need to acquire a stablecoin like USDT or USDC. These digital tokens are pegged to the US dollar, meaning one token always equals one dollar. This stability is what makes them ideal for remittances, as the value won't fluctuate wildly between the time you buy and the time your family receives it.

To keep costs low, choose a regulated exchange that supports direct fiat on-ramps. Platforms like Coinbase or Kraken allow you to link a bank account or debit card to buy stablecoins instantly. Bank transfers usually have the lowest fees, though they may take a day or two to clear. Debit cards are faster but often carry higher processing charges.

Security is paramount when moving real money. Ensure the exchange is registered with relevant financial authorities in your jurisdiction. Avoid unregulated peer-to-peer (P2P) markets unless you are an experienced user, as these carry a higher risk of fraud. Once your fiat currency is converted, the stablecoins will appear in your exchange wallet, ready for transfer.

Step 2: Transfer to a LATAM-friendly wallet

Once your stablecoins are on a regulated exchange, the next move is getting them into a wallet that supports local withdrawals. This step is the bridge between your digital assets and the recipient's bank account or mobile money service. A "LATAM-friendly" wallet is one that integrates directly with local payment rails, such as Binance Pay, local P2P platforms, or fintech apps like Nequi and Daviplata in Colombia, or Mercado Pago in Argentina.

Choosing the right wallet matters because it determines how fast and cheap the final delivery is. If you send funds to a generic self-custody wallet like MetaMask, you will still need a second exchange or a crypto debit card to convert them to local currency. This adds friction and extra fees. Instead, use a wallet that acts as a gateway to the local banking system.

1. Select a wallet with local payout integration

Look for platforms that explicitly support "P2P trading" or "crypto-to-bank" transfers in the recipient's country. Binance is the most common choice because it supports dozens of local currencies and payment methods. Other options include Bybit or local fintechs that hold crypto licenses. Ensure the wallet you choose allows you to receive USDT or USDC directly without converting it to a volatile asset first.

2. Verify the recipient's wallet address

Before sending, confirm the exact network (chain) the recipient uses. Most LATAM wallets support TRC-20 (Tron) or ERC-20 (Ethereum) for USDT. TRC-20 is usually preferred for lower fees and faster settlement. Sending on the wrong network can result in lost funds. Ask the recipient to generate a new address specifically for this transfer to avoid confusion with previous transactions.

3. Execute the transfer

Initiate the withdrawal from your exchange to the recipient's wallet address. Start with a small test amount if this is your first time using this specific wallet. Once the test confirms successful delivery, send the remaining balance. Keep the transaction hash (TXID) handy in case the recipient reports non-receipt.

4. Confirm receipt and payout

The recipient should receive the stablecoins in their wallet within minutes. They can then use the platform's internal "Sell" or "Cash Out" feature to convert the stablecoins to local currency and withdraw to their bank account or mobile wallet. This process is often faster and cheaper than traditional SWIFT transfers, which can take 3-5 business days and charge 1-3% fees.

Select a platform like Binance or a local fintech that supports direct bank withdrawals in the recipient's country. Avoid generic wallets that require a second exchange to cash out.

Confirm the recipient uses TRC-20 or ERC-20 for USDT. TRC-20 is typically cheaper and faster. Double-check the address character by character to prevent loss.

Transfer a small amount first. This verifies the wallet is active and the payout method is correctly configured before sending the full remittance.

Once the test succeeds, send the remaining balance. The recipient can then convert the stablecoins to local currency via the platform's integrated banking rails.

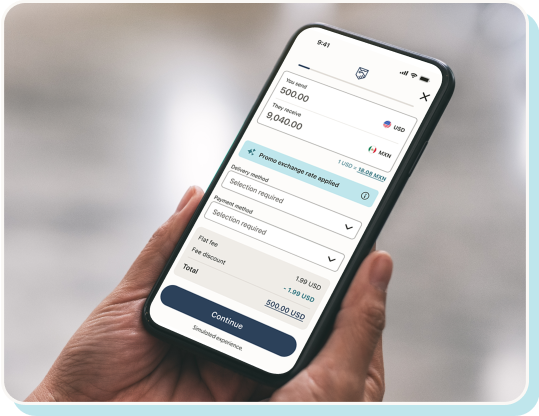

Step 3: Convert to local currency for the recipient

Send Money to Latin America With Stablecoins works best as a sequence, not a scramble through settings. Do the minimum first: confirm compatibility, connect the core hardware, update only when needed, and test the result before adding optional features. That order keeps the task understandable and makes failures easier to isolate. After each step, pause long enough for the interface to finish syncing. Many setup problems are timing problems disguised as configuration problems. If the same step fails twice, record the exact error, restart the smallest affected piece, and retry before moving deeper.

Avoid common crypto remittance mistakes

When you send money to Latin America 2026 using stablecoins, the blockchain network is the highway, not the destination. Choosing the wrong one is the most frequent and costly error. Sending USDC via Ethereum (ERC20) can cost $5 to $20 in gas fees for a $50 transfer, effectively destroying the value of the remittance. Instead, use low-cost networks like Tron (TRC20), Solana, or Polygon. Always verify the recipient’s wallet address supports the specific network you select before hitting send.

Exchange rate slippage is the second silent killer. Many platforms advertise a "mid-market rate" but apply a hidden spread during the final fiat conversion to the recipient’s local bank account or mobile wallet. This spread can range from 1% to 3%. Compare the final amount the recipient receives against the raw exchange rate. If the difference is large, the platform is charging you through the spread rather than a transparent fee.

Never ignore the destination country’s regulatory requirements. Some Latin American countries have strict limits on crypto-to-fiat conversions or require additional identity verification for larger transfers. Ensure the recipient’s bank or payment provider accepts the specific stablecoin you are sending. A transaction that fails at the cash-out stage ties up funds and creates unnecessary friction for your family.

FAQ: Stablecoin remittances in 2026

Is the 1% remittance tax applied to stablecoin transfers?

No. The 1% remittance transfer tax, which begins on January 1, 2026, only applies when the sender provides cash, a money order, a cashier's check, or other similar physical instruments to the transfer provider IRS. Because stablecoin transfers are digital and do not involve physical payment instruments, they fall outside the scope of this tax. This makes sending money to Latin America 2026 via crypto a more cost-effective option for avoiding this new levy.

How are stablecoin remittances taxed for the sender?

The 1% tax is a specific fee on the transfer method, not a general income tax. However, you must still report any capital gains if the stablecoin increased in value between the time you acquired it and the time you sent it. Consult a tax professional to understand how digital asset transactions impact your personal tax liability in your jurisdiction.

Is it safe to send money to Latin America 2026 using stablecoins?

Stablecoins are generally safer than cash because the blockchain provides a transparent, immutable record of every transaction. Unlike cash, which can be lost or stolen with no recourse, digital transfers are traceable. However, safety also depends on your security practices: use reputable exchanges, enable two-factor authentication, and double-check recipient wallet addresses before confirming any transfer.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!